Ultimate Products (ULTP)

A future hanging in the balance....

Ultimate Products has many of the attributes associated with a quality company: a capital light business model, a long history of sales growth, and an experienced management team of owner-operators.

Yet, recently the business has been going through a difficult patch. A relatively small drop in sales and profitability has punished the share price, which has fallen by two thirds.

If these issues are temporary, then it’s an excellent time to learn more. It could even be a good entry point for the patient investor….

Ultimate products is a consumer goods company that sources, designs, and distributes products for the home. It’s based in Oldham, near Manchester, and is listed on the main market of the London Stock Exchange.

Many of the brands owned by Ultimate Products are household names and can be found in kitchens and bathrooms across the UK.

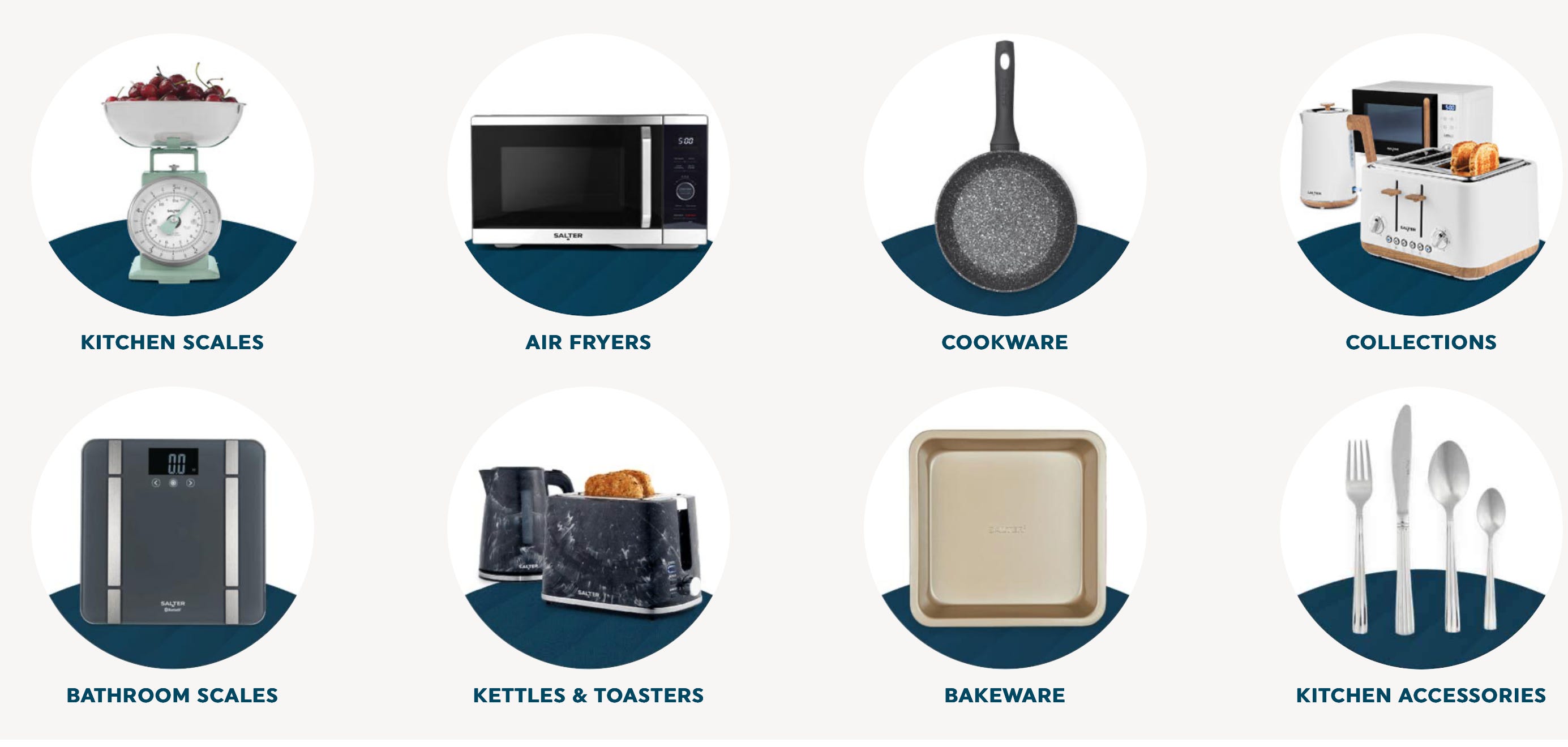

Salter (~40% total sales). The UK’s oldest houseware brand with a history dating back to the 18th Century. Just under half of Salter’s sales come from its measurement business, where the brand has a ~60% market share in the UK. The remaining sales are split between cookware, kettles, toasters, and air fryers.

Beldray (~20% total sales). Beldray’s history dates back to the late 19th century. Today, it sells laundry items (irons, airers, and baskets), vacuum cleaners, and various cloths, brushes and dusters.

Supporting Brands (~20% total sales). Ultimate products owns 9 supporting brands. The largest of which are Progress (cookware), Petra (coffee makers), Kleeneze (cleaning, heating and cooling), and Intempo (audio products).

Other (~20% total sales). Ultimate Products has a licence deal with Russell Hobbs to sell cookware (~10% total sales) and a stock clearance business (~10% total sales).

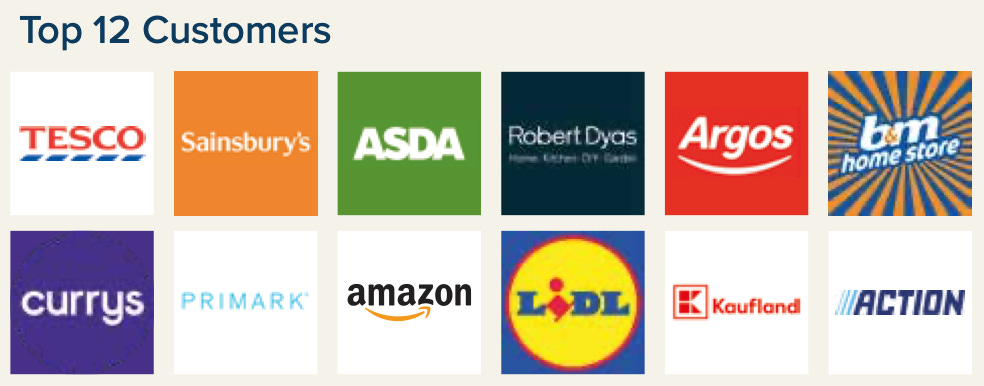

Ultimate Products’ customers are broken down into four categories: Supermarkets, Discounters, Online and Other (think independent retailers and larger multiples).

The three largest are each responsible for ~15% of total sales, with no other customer making up more than ~10% of total sales.

The business quality

Simon Showman, one of the original founders, describes Ultimate Products as providing John Lewis products for the Asda price. For those less familiar with UK retail, Ultimate Products sells value (or relatively cheap) household items to the mass market.

Ultimate Products designs and distributes, but it doesn’t own any factories or manufacturing facilities. This more capital intensive aspect is predominately outsourced to China. Where there’s both an office and showroom based in Guangzhou.

The pricing strategy is particularly clever.

Instead of using its own brands to drive a premium. The price is purposely kept low in order to drive volume. Essentially, products are priced at a level that ensures the customers (supermarkets and discounters) earn the same margin as they would by selling their own branded products.

When executed successfully, this is a win for retailers, who make a decent margin, consumers, who get a lower cost product, and Ultimate Products, who continues to grow.

In some ways, this reminds me of the scale economies shared principle that has been so successfully employed by global behemoths such as Costco and Amazon.

In theory, as Ultimate Products grows, unit costs decrease. With margins maintained, and costs decreasing, price discounts can be handed back to customers. Thereby, creating a virtuous cycle of improving volumes, customer loyalty, and market share. All of which, help maintain a competitive advantage.

Historically, there is some evidence of this competitive advantage, given the sustainably high Returns on Tangible Capital Employed.

The Drivers of Growth

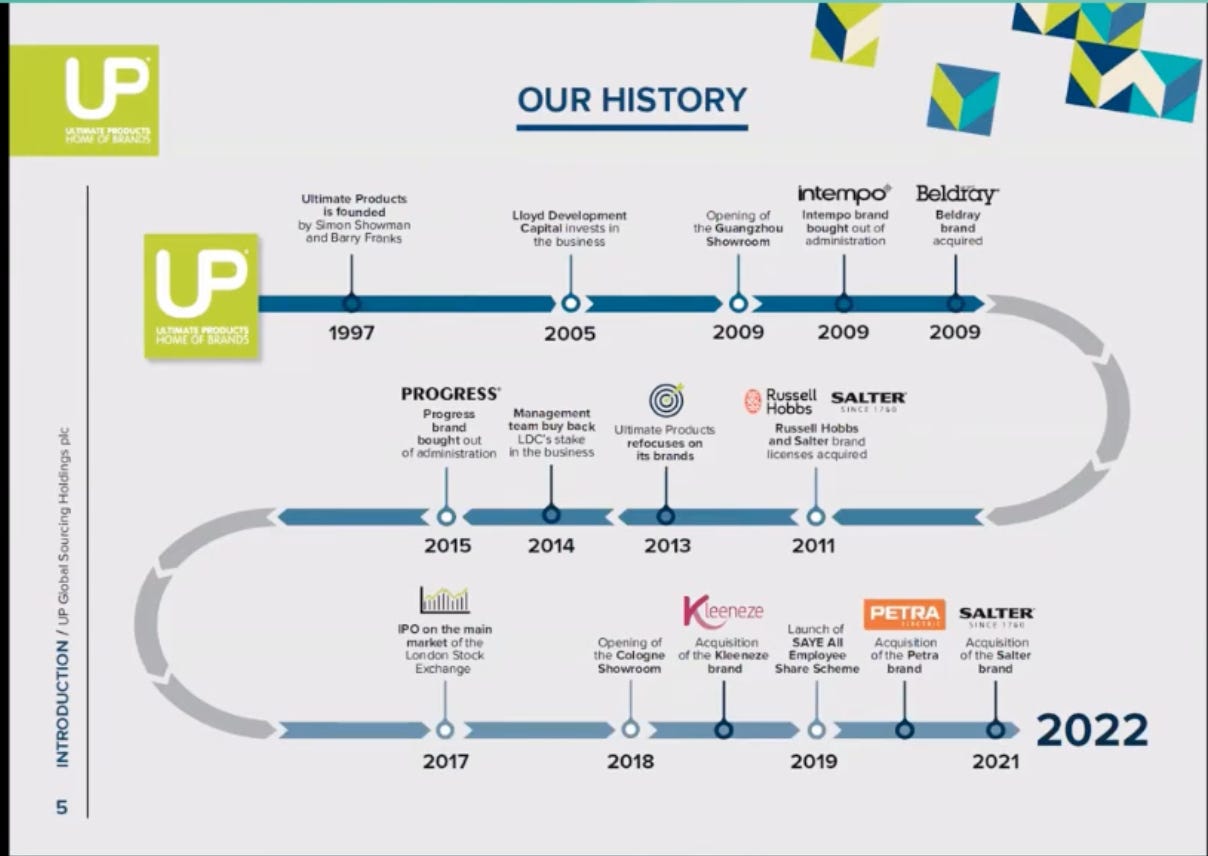

Founded by Simon Showman and Barry Franks in 1997. Ultimate Products started out as a stock clearance business, sourcing discontinued and excess inventory from countries such as Portugal, Vietnam, and China.

In 2009, the trajectory of the business shifted towards branded products. When management purchased two brands (Intempo and Beldray) out of administration. Both were quickly turned around and further brand acquisitions followed.

The sales growth of branded products really accelerated following Ultimate Products’ IPO in 2017. After which, fully owned brands became the driving force behind the company’s growth.

Another positive, has been the improving diversification across the customer base.

Prior to IPO, customer concentration was high because the majority of branded sales were to a few large discount retailers based in the UK.

To combat this issue, the management team have successfully targeted supermarkets and online channels. Both of which have grown to represent a material portion of total sales.

Growth has also come from geographical expansion into Europe. Where management implemented a land and expand strategy focused on Germany, France, and Holland. Today, the largest European clients include the German supermarket Kaufland, and the Dutch discount retailer Action.

With almost ten times the population, Europe remains a significant opportunity, and sales continue to grow.

The Management

At the helm of Ultimate Products is an experienced team of owner-operators.

Current and former executives still own over 40% of the business. Simon Showman, the Chief Commercial Officer and one of the original founders, is the largest shareholder with ~20% of Shares Outstanding. The other founder, Barry Franks, owns ~12%, and the current CEO, Andrew Gossard owns ~9%.

They have a clear capital allocation policy that distributes 50% of post-tax profits to shareholders through dividends.

Occasionally, these dividends are supplemented by share buybacks. But only when Net Bank Debt is around, or below, a target of 1 times EBITDA.

Acquisitions are infrequent and opportunistic. Most have been small (<£1 million), purchasing struggling brands out of administration.

The exception being the Salter acquisition in 2021. Where management paid £34 million for the entire brand (this included the measurement business with sales of ~£17 million and EBITDA of ~£3 million but it also removed ~£1.5 million that was previously being paid to Salter as a licence fee).

To get a better understanding of the management team, I’d highly recommend listening to the historic presentations on the Equity Development website. The management team are fairly open and I found their presentations incredibly useful.

The Valuation and Risks

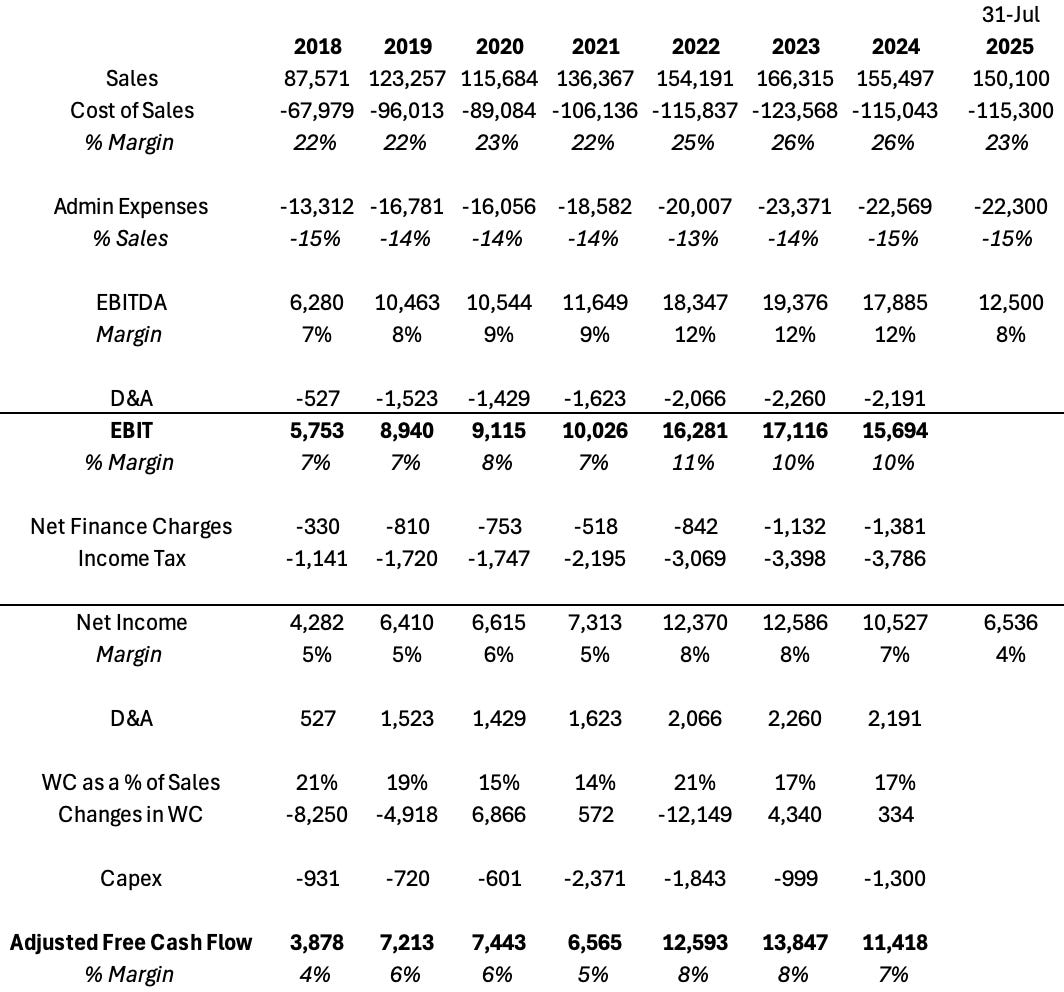

At ~63p per share, the current market capitalisation is ~£55 million. So including the Net Debt of ~£15 million, gives us a current Enterprise Value of ~£70 million.

If we compare this to Sales of ~£150 million and Operating Profits of ~£10 million in the year ending 31st July 2025. We get a reasonable (but fairly unexciting) valuation of ~7x Operating Profit.

Yet, if we wanted to be more optimistic, there’s good reasons to believe that Ultimate Products can earn sustainably higher Operating Profits. Here’s a few of them:

Decreasing freight costs. Due to the closure of the Red Sea, containers have been taking an average of 15-20 days longer to traverse the Horn of Africa. In FY 25, this has had the temporary effect of reducing Operating Profit by over £3 million due to the additional freight costs (See pre close trading update - 13 August 2025)

Historical Operating Margins. In all of the previous three years, Ultimate Products earned Operating Margins of over 10%, compared to 7% in FY25.

European growth. The UK market is expected to continue shrinking and any rebound is hard to predict. However, Europe remains a growth engine and a significant opportunity for the future.

Management’s focus on efficiency and automation. Profitability, measured on a per employee basis, is a key efficiency metric for the management team. Who have been employing process automation and Artificial Intelligence before anyone even heard of ChatGPT!

There’s also reasons to be cautious.

Recently, the Net Debt position has been growing and currently sits at ~£15 million. Although still low, at less than ~2 x Operating Profit, the situation could rapidly deteriorate if earnings were to shrink further.

On this point, I’ve slowly become more comfortable (rightly or wrongly!) due to the strength of the Balance Sheet. As of the latest report (on 31st January 2025), Ultimate Products held increased inventory, of ~£40 million, which more than covers the entire Net Debt position.

In addition, around a third is categorised as Sold Stock and includes a Firm Purchase Order from a large retail client. In practice, this lower risk form of inventory is highly likely to convert into cashflow over the next few months.

In summary, the valuation seems cheap and the shares look oversold. There’s a long history of growth alongside sustained profitability and cash flow generation. I also like the quality of the business and the alignment of the management team.

Therefore, I’ve bought a starter position (amounting to ~5% of my portfolio) and will be following along closely!

Thanks, as always, for your interest and support!

Disclaimer. This article is for informational purposes only, and should not be seen as investment advice. Please do your own research before investing in any company mentioned.

Financial Model: