Reckon (RKN) Update #1

A falling share price meets improving fundamentals

The original article remains one of my most popular.

Though as an investment, Reckon has been a complete dud. Particularly, over the past six months when the share price has dropped by around a quarter.

Granted, this slump resonates with other small software companies, hit by growing concerns over the impact of AI.

However, in this case, the tumbling valuation is completely at odds with the fundamentals. Since I introduced Reckon in 2023, sales have grown in every year and Operating Profit (and Free Cash Flow) has roughly doubled.

There’s also an impending catalyst. By the 31st December 2029, management intends to realise significant value for shareholders.

As I wrote in my original article:

The CEO, Sam Allert, is heavily incentivised to continue this trend and divest the remaining two businesses. Under a recently implemented incentive scheme, he receives a payout only if shareholder distributions over the next six years (to the end of 2029) reach A$150 million (over twice Reckon’s current Enterprise Value). If payouts reach A$300 million, Sam Allert receives almost ~A$6 million, equivalent to 9 times his base salary!

To understand what’s happening, let’s take a closer look at the two businesses.

Accounting Software

As I highlighted in my original post, the Accounting Software division is the obvious source of remaining value, generating over three quarters of Reckon’s sales and the entirety of the company’s profit.

Results have been steady for the past decade.

However, the same problem persists. A sale cannot take place until all customers are migrated from a legacy software product, called Reckon Accounts, onto a newer product, called Reckon One.

In preparation, management has been closing the functionality gap between these two products. In their Full Year 2025 Presentation, they estimated ~75% of Reckon Accounts customers could be migrated using the current Reckon One features, rising to ~90%, by year end.

Given these advancements, the migration has started. Initially, at ~100 to ~150 subscribers per month, who serve as a test case and help improve processes. Over the course of this year, the numbers will ramp up significantly. With the bulk of the migration taking place in 2027.

If all goes to plan, by the end of 2028 management expect to have migrated all ~41,000 subscribers, who currently represent ~64% of Accounting Software sales.

Obviously, at this early stage it’s difficult to judge the migration’s success (or otherwise). So to keep you informed, I’ll update this chart (at least annually) using the Notes section of Overlooked and Undervalued:

Legal Software

As for Legal Software, I was unsure back in 2023 whether a sale of this business was even possible. It had been losing money for years and a wind-down seemed increasingly likely.

Recently however, the situation has dramatically improved. After years of losses, management are finally expecting to generate Free Cash Flow. A milestone that makes a sale much more likely and represents a material boost to the overall investment case.

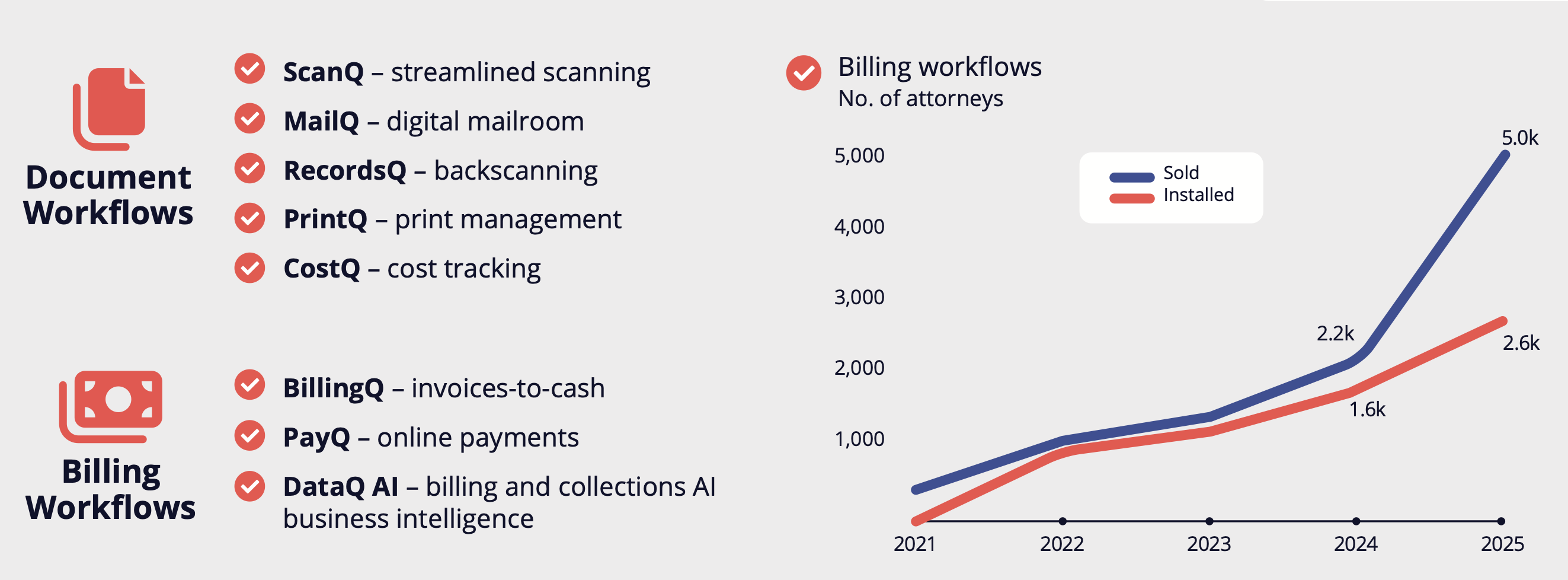

Historically, this business sold Document Management software to the legal industry - used for tasks such as scanning, printing, digitalising physical mail, and cost tracking. As you might imagine, this kind of software isn’t exactly an exciting growth story. Customer relationships were solid but sales had been languishing for a decade.

So in 2020, Reckon acquired a large stake in Zebraworks - a software startup developing a Billing Workflow tool for the legal industry. Given the limited competition, management believed that Zebraworks had the potential to become a market leader.

The other attraction was the management team. Zebraworks was led by Bill Bice, the founder of ProLaw, the leading Practice Management System within the legal industry. Bill Bice is almost uniquely placed to achieve seamless integration of Reckon’s products within Practice Management Systems - a necessary task in order to stay relevant.

Under his leadership, the entire business (including Document Management) was rolled up into a new company called nQ Zebraworks. This clever combination allowed for the cross-selling of Billing Workflow products to Reckon’s already established customer base, which includes 12 of the 20 largest law firms globally and 40% of the AmLaw 200.

This plan is working. Divisional sales grew by 12% over Full Year 2025, driven by a doubling in Billing Workflow sales, which reached ~A$1 million in Annual Recurring Revenue (ARR). Concurrently, divisional losses halved to ~A$2 million.

Going forward, we can expect these improvements to continue due to the high levels of demand for Reckon’s Billing Workflow tools. With fixed overheads and sales continuing to grow, management anticipate Free Cash Flow generation by year end.

Who knows, this division might be worth something after all!…

At A$0.42 per share, Reckon’s current Market Capitalisation is ~A$47 million. Including ~A$8 million of Net Debt, the Enterprise Value is ~A$55 million.

Again, if we compare this solely to the Accounting Software division, which in Full Year 2025 had sales of ~A$49 million and Operating Profits of ~A$14 million, the current valuation remains low, verging on ridiculous.

Granted, there’s a migration going on, which remains a significant risk. However, there’s good reasons to expect customers to stay:

Similar functionality and price. Reckon One has been developed to match the functionality of Reckon Accounts and will be available at a similar price.

The alternatives. When compared to MYOB and Xero, Reckon’s products are generally cheaper and better regarded by customers (evidenced by Reckon’s higher Trustpilot score).

Complexity. The users of Reckon Accounts are generally larger, more complex businesses, which makes it more difficult (though not impossible) to switch.

Strong relationships. Past churn rates have been low at ~6-8% and customer relationships stretch over years and even decades.

Dedicated migration team. A dedicated team will help clients through the transition and follow up with customers to ensure they are comfortable with the new product.

As for the Legal Software division, it adds optionality. If the current growth levels are maintained, a sale of this business would be material. If not, it’s unlikely to represent a continuing drag on consolidated results.

At the end of the original article, I wrote that I remain confident that the true value of the Accounting Software business will be unlocked - an event I’d expect to result in a valuation (or distribution) that’s multiples of the current price.

For me, this hasn't changed. Over the past few years, the opportunity has gradually improved, whilst the share price has continued to fall.

A disconnect between price and value? I certainly think so.

(My current position is ~10% of the portfolio.)

Disclaimer. This article is for informational purposes only, and should not be seen as investment advice. Please do your own research before investing in any company mentioned.