Palace Capital (PCA)

The cheapest property company in the UK....oh....and it's almost debt free.

So, I wasn't planning on sending something out so soon after my last post - it normally takes me months, rather than weeks, to find a worthwhile idea. But, I think the recently announced sale of Palace Capital’s industrial portfolio is worth sharing. This change not only increases expected returns for shareholders, but it also significantly reduces debt - a rare combination. Especially, when nobody seems to have noticed and the share price has hardly moved.

Honestly, I’m a tourist in the world of property investment. I generally steer clear of Real Estate Investment Trusts (or REITs) because of a few attributes that often result in low shareholder returns. Namely, management teams that are well compensated but with very low insider ownership. Alongside, growth that almost entirely funded by diluting shareholders and increasing leverage.

Palace Capital is a good example. Founded in 2010, without a single investment property, the portfolio peaked at over 50 buildings in 2019, valued at ~£260mm. The two founders started as large shareholders. But as Palace Capital grew, equity financing diluted their ownership down to less than 2% of shares outstanding. Whilst at the same time their compensation increased five fold to well over £1mm. Shareholders didn’t come out quite as well - over the last decade Total Shareholder Returns (including dividends) were a meagre ~3% per year!

Today, Palace Capital owns 29 buildings - over half are offices with the remainder split between leisure (cinema complexes) and retail (city centre shops, supermarkets and warehouses). All are based outside of London, in major university towns and cities, and located close to train stations and transport hubs.

Here are six of the highest income properties:

I started buying shares around October 2022. At the time, Peter Gyllenhammer, a Swedish activist investor, had built an ownership stake of over 10% and both founders had left the company (I expect they were pushed!). A new board, led by an Executive Chairman was employing a very different strategy:

The Board's strategy is to focus on maximising cash returns to shareholders, whilst continuing to remain mindful of consolidation in the Real Estate sector.

Properties were being sold, debt was being reduced, and the company had started buying back shares at a large discount to book value. As property sales accelerated, the share price hardly moved. But, prospective returns are increasing.

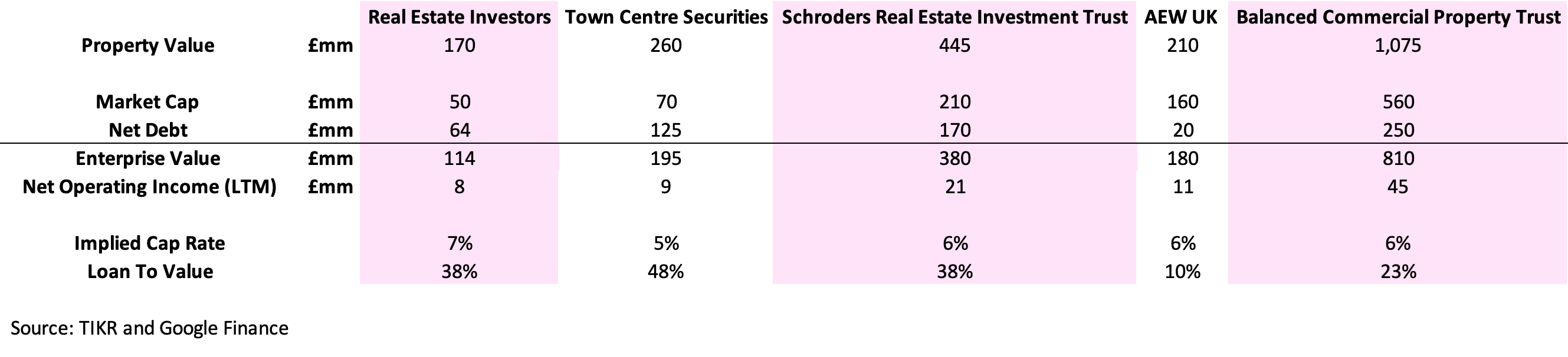

To keep this post short, I’m not going to attempt a lengthy valuation breakdown of every building. Instead, I’ll focus on Palace Capital’s Implied Cap Rate (Operating Income / Enterprise Value).

To calculated this, we need Palace Capital’s Net Debt and annual rental income. The most recent annual report (dated 31st March 2022) gives us a Net Debt of £73mm and annual rental income of £15.2 mm. But this was over a year ago, and multiple property sales have happened since then. Last week’s announcement provided a good summary:

£21mm in cash received from the sale of 8 Investment properties and a Supermarket (with an annual rental income of £1.2mm).

23 residential apartments in York sold for £10mm.

Contracts exchanged for the sale of 6 Industrial Properties for £34mm (with an annual rental income of £2.2mm).

Rent reviews and new lettings increased annual rental income by £1.1mm.

Taking account of these changes, normalised rental income has reduced to ~£13 mm per year but Palace Capital is close to being debt free. Especially, if you include another £10mm expected from the sale of the last remaining apartments in York.

At £2.3 per share, the market cap is ~£100mm. Book value is ~£155mm. Assuming no Net Debt and an annual rental income of £13mm, the property portfolio has an impressive 13% yield and after including £4mm of central costs, Palace Capital trades at a 9% Cap Rate.

Searching around in the UK, I could not find a single REIT trading anywhere close to a 9% Cap Rate. In fact, comparing Palace Capital to five similar companies, the average is around 6%. A figure that suggests Palace Capital’s shares could be worth at least 50% above the current price, or over £3 a share.

Yet, whatever the relative value, I’m highly confident that within a year, Palace Capital will have almost no debt and be earning an Implied Cap Rate (and Dividend Yield) of close to ~10%. But’s that’s not all. This income stream will likely increase over time because of ongoing rent reviews, where contracts are tied to inflation (normally capped at ~2-3% per year).

But Adrian, you do realise this is office space? It’s also a pretty mixed bag with some low grade dross. Working from home is killing demand, energy efficiency standards are rising, and occupancy rates are reducing across the sector.

This is all true. Yet ultimately, I think the downside is well protected. In the company’s offices, current occupancy rates sit at 85% (with the remainder of the portfolio at over 95%). But, let’s imagine an outpouring of clients reduces office occupancy to say 50%, a likely worst case scenario. Operating Income would drop, but due to the mix of properties, only to ~£6-7mm. Thereby, leaving a debt free Palace Capital trading at a reasonably average ~5-6% Cap Rate. A far from awful outcome.

In summary, Palace Capital represents the chance to earn a roughly 10% annual dividend on a debt free property company, with minimal downside. Maybe, you’re finding much better opportunities, but to me, this seems like a bargain! I remain somewhat sceptical of the wider sector and the opportunities for the long-term investor - but hey, there’s always one exception to every rule!? Right?

Disclaimer. This article is for informational purposes only, and should not be seen as investment advice. Please do your own research before investing in any company mentioned.

Thanks for this, as a holder of RLE this is an interesting comp. There seems to be £18m debt proforma all the disposals and selling the remaining flats will only clear £8m of that if they get the same price per flat as they got for the others. So £9m (After central costs but before the small remaining interest) / (100m mcap + 10m debt post flat sales) = 8.2% yield. Which is good but not as exceptional as it looked.

Put another way, it trades on 75% of NAV or 78% of GAV, which isn't terribly discounted. RLE, more levered, is <50% of NAV and c. 67% of GAV.

The admin costs are an intolerable burden on these subscale-and-shrinking REITs, £4m here and over £3m at RLE. They should be taken out or at least merge for some scale.

Thank you for a very interesting write up. What are the realistic chances that the management will go to an extreme unlevered scenario with the company? I believe that unless that has been directly communicated to shareholders (I am not aware of this) the most likely scenario will be one with some leverage - probably lower than currently which will not help crystalize the undervaluation in this. Worst case they get involved in some development project and all the upside is gone. Interested to hear your thoughts on this. Thanks